The Sandwich Generation Trap: Why Indian Millennials Are Getting Two Sets of Investment Ideas And Missing a Third Conversation Entirely

Introduction

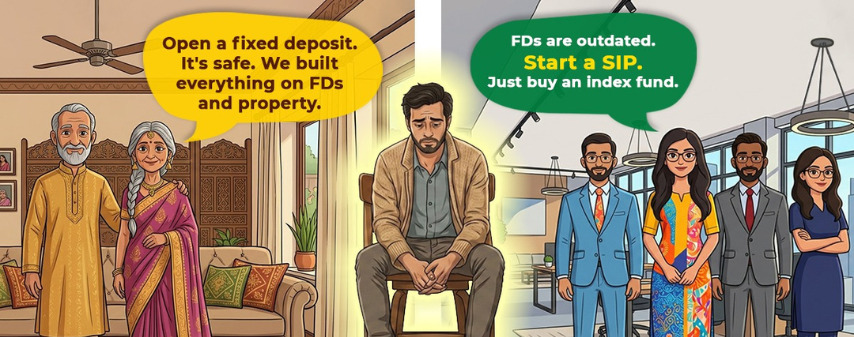

For Indian millennials, the FD vs mutual funds debate isn’t just financial – it’s personal. It’s the first week of the month. Your salary lands. Before you’ve made a single decision, the advice starts flooding in from two very different directions.

Your parents say: “Fixed Deposit. Property. Gold. It’s safe. We built everything on this.” Your Instagram feed says: “FDs are outdated. Open a SIP. Buy the Nifty 50 index fund and forget it.”

You nod to both. The money sits in your savings account. Weeks pass. This hesitation — this paralysis between two eras of financial thinking is the invisible tax on your wealth.

This is what we call the Sandwich Generation problem. Indians are uniquely caught between their parents’ proven-but-dated financial playbook and a new-wave narrative that dismisses everything their parents built. Both sides have a point. Both sides are missing something.

This article doesn’t pick a side. It builds the case for a third, more important conversation grounded in what the data says in 2026, not what worked in 1995 or went viral last month.

Fixed Deposits for Indian Millennials: Safe, But Are the Returns Enough?

Let’s start with Fixed Deposits. Your parents were not wrong to trust them. India’s banking FD system is DICGC-insured up to ₹5 lakh per depositor per bank, backed by a subsidiary of the RBI. The returns are predictable. For deposits within DICGC insurance limits, the risk of permanent capital loss is relatively low, though access and liquidity may still depend on resolution timelines.

So the question was never really about safety. It was always about whether safety alone is sufficient over a 10–20 year wealth-building horizon. And that’s where the numbers deserve a closer look.

FD Interest Rates India: What Are They Actually Paying in 2026?

As of April 2026, FD rates across major banks sit between 5–7% (Source: Mint). At the same time, India’s average CPI inflation over the last decade has hovered around 5%, according to MOSPI data meaning an average household has had to spend roughly 5% more on goods and services every single year, year after year.

When you place those two numbers side by side, the picture becomes clear. FDs are traditionally considered safer instruments, but they may not always generate returns that significantly outpace inflation. That distinction matters enormously when you’re trying to build wealth, not just preserve it.

Property Investment India: Why the Math Has Changed for Millennials

Property built genuine, generational wealth for Indian families. Your parents likely bought a home in the late 1980s or 1990s at prices that today seem remarkably low. But the conditions that made possible low entry prices, rising middle-class incomes, limited supply competition are structurally different today, and the numbers reflect that shift clearly.

What Has Actually Happened to Prices?

In Delhi-NCR, residential prices have risen over 81% in just five years, far outpacing salary growth that averaged 8–10% annually over the same period (Source: Week). To put that in practical terms: a home that cost ₹50 lakh in Noida in 2020 costs approximately ₹90–95 lakh today. The salary that was meant to fund that purchase has grown by perhaps 40–50% over the same period.

For many middle-income households in earlier decades, home ownership was often achievable at materially lower income multiples than it is today.

Applying old rules to new prices is where the trap begins. This doesn’t mean property is a poor long-term asset. It means it requires significantly more capital, longer timelines, and more careful planning than it did for the previous generation and deserves honest analysis rather than assumption.

Mutual Funds via SIP: Real Data on What Indian Millennials Are Actually Doing

Something significant has happened in Indian financial markets over the last five years that makes this conversation more urgent than ever. According to AMFI’s official March 2026 data, the mutual fund industry’s AUM now stands at ₹73.73 lakh crore, with 9.72 crore active SIP contributing accounts. Monthly SIP contributions reached ₹32,087 crore in March 2026, and equity schemes have recorded 61 consecutive months of net positive inflows since March 2021.

These are not abstract numbers. They represent millions of Indian households, many of them first-generation equity investors choosing to stay invested through market ups and downs, month after month. Systematic investing through SIPs creates the discipline of contributing through market cycles, which over long periods has historically helped investors participate in equity market growth. For someone with a 15–25 year investment horizon, equity mutual funds deserve a meaningful role in their portfolio.

But the internet has a tendency to simplify nuanced ideas into easy slogans. “Just buy the Nifty 50 index fund and forget it” is one of them. That framing creates confusion rather than simplifying things. Investing works very differently depending on where an approach holds up and where it breaks down. That’s the difference between a strategy and a prescription.

Active vs. Passive Funds: A Decision Based on Context, Not Conviction

As the financial market is dependent on many factors, giving any general statement does not hold any merit on it. There have been periods where certain actively managed funds have shown relative resilience compared to benchmarks. However, this varies across market cycles and fund categories.

There have been market phases where certain actively managed small-cap strategies have shown different downside and return outcomes relative to their benchmarks. However, these outcomes have not been uniform across market cycles, fund categories, or time periods, and are influenced by fund selection, costs, and portfolio construction (Source: ValueResearch).

Why? A Nifty 50 stock has 25–30 analysts on it. A quality small-cap company might have two. That information gap is one reason active management is often evaluated in less efficiently tracked market segments, though outcomes remain dependent on market conditions, costs, and portfolio execution.

The active-vs-passive question does not have a single universal answer. The right approach depends on the asset class, market maturity, investment horizon, and cost structure of available options. A blanket rule applied across a heterogeneous market leads to gaps in portfolio construction.

The Third Conversation No One Is Having

Here is where both the FD generation and the Instagram-investing generation fall short. The real question is not “which instrument is best?” The real question is: best for what?

Every financial goal carries a different time horizon, a different risk profile, and a different ideal instrument. Treating all your investments as a single bucket or choosing instruments based on what feels safe or what performed well recently is how people end up with money that isn’t aligned with their actual needs.

The greatest risk isn’t the market. It’s the lack of alignment.

The real mistake isn’t a lack of intent, it’s a lack of alignment. Not knowing which asset class is appropriate for which goal means that even well-intentioned investors can find themselves unable to grow their wealth toward the milestones that matter most to them. We often treat investments like a single bucket when they should be a toolkit, with each tool matched to a specific job.

In parts of India’s mid- and small-cap market, where information coverage and market efficiency can vary, active management may be considered as one approach depending on portfolio objectives and risk tolerance. In other parts of the market, low-cost passive exposure may serve better. Neither answer fits every situation.

Your parents built wealth through consistency using the tools and knowledge that were available to them and that they genuinely understood. The tools look different today. The discipline is the same. Rather than getting stuck in the Sandwich Generation Trap pulled in opposite directions by two incomplete narratives, the goal is a clear resolve to invest according to your individual risk profile, your financial goals, and your investment horizon.

Clarity is the first step toward better financial decision-making.

In situations like these, the role of an AMFI-registered Mutual Fund Distributor can be to support investors with more structured financial decision-making. We begin by understanding our clients’ goals and future objectives to gain a clear picture of their current investment position and the financial milestones they aim to achieve. Based on each client’s risk profile, financial goals, and investment horizon, we create client-specific investment strategies. Through in-depth research and analysis of both the market and mutual fund performance, we aim to align investment decisions with long-term financial goals.

Data Disclaimer: Data referenced in this article is based on publicly available sources including AMFI and third-party research platforms, and is for informational purposes only. This article does not constitute investment advice. Please consult a qualified financial advisor before making investment decisions.

Note: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. The past performance of the schemes is neither an indicator nor a guarantee of future performance.

Leave a Reply