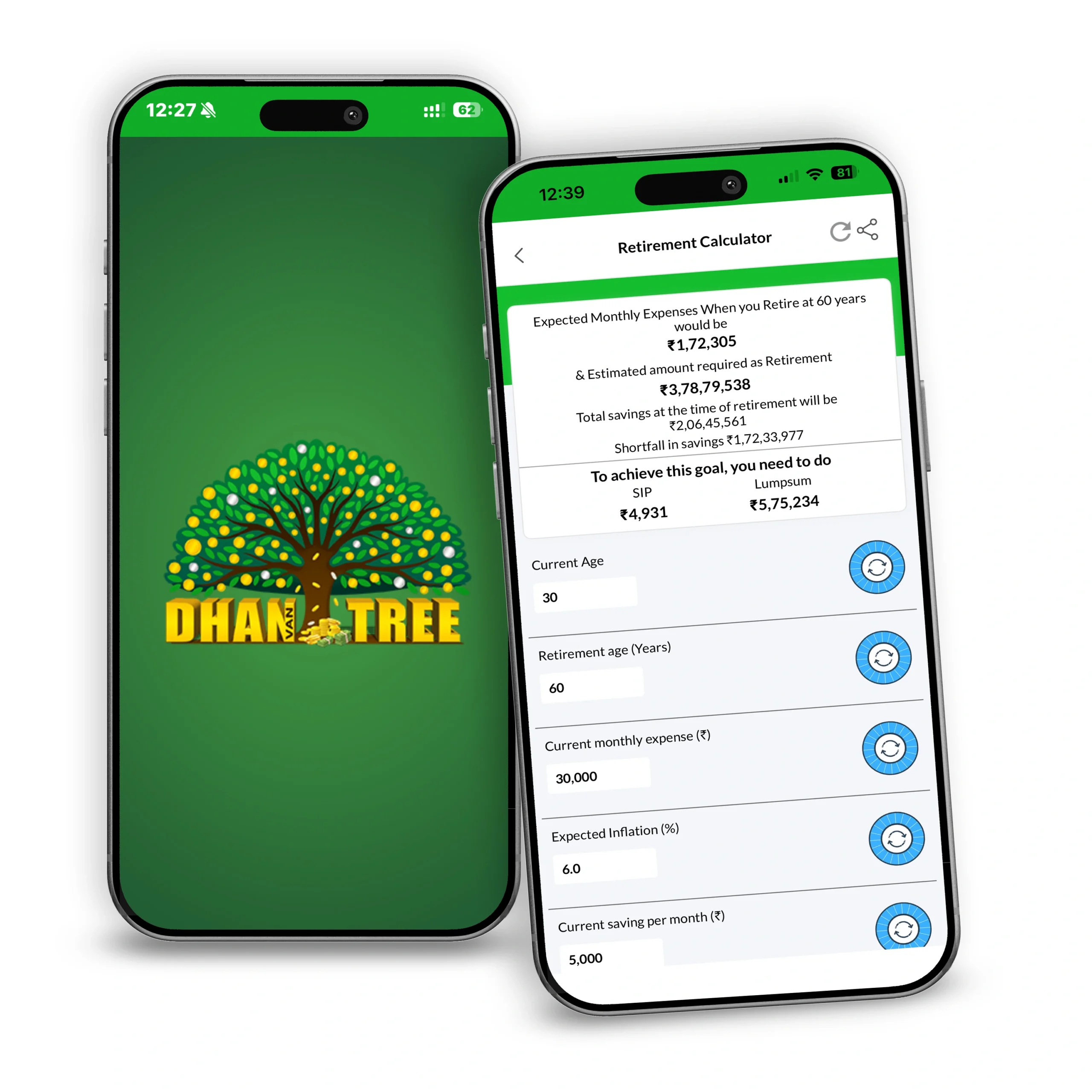

Retirement Calculator

Retirement Calculator

Retirement Calculator

Estimate retirement corpus, savings shortfall, SIP and lumpsum required.

Current age should be at least 20 years. Retirement age should be maximum 80 years. Pre-retirement return should be less than or equal to 30%. Post-retirement return should be less than or equal to 30%.Expected Monthly Expenses at Retirement: ₹0

Estimated Retirement Corpus Required: ₹0

Total Savings at Retirement: ₹0

Shortfall in Savings: ₹0

SIP Needed: ₹0

Lumpsum Needed: ₹0

Disclaimer: This calculator is for illustration purposes only. Mutual fund investments are subject to market risks. Returns are not guaranteed.

What is a Retirement Calculator?

A risk profile quantifies an individual’s tolerance for risk. Each person’s risk tolerance varies based on factors like disposable income and age. Understanding a person’s risk profile helps both the investor and a financial advisor design an investment portfolio with an appropriate mix of assets that aligns with the individual’s risk tolerance.

Risk tolerance is the degree to which an investor is willing to accept risk or volatility in their investment returns. For instance, a risk-averse individual prefers to maintain the value of their portfolio rather than seeking high or moderate returns. Conversely, a risk-seeking individual is willing to endure market fluctuations for the chance of achieving substantial returns.

Disclaimer

- Past performance may or may not be sustained in future and is not a guarantee of any future returns.

- Please note that these calculators are for illustrations only and do not represent actual returns.

- Mutual Funds do not have a fixed rate of return and it is not possible to predict the rate of return.

- Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.

All Your Financial Tools, Right in Your Pocket.

Download Dhanvantree App

From onboarding to portfolio tracking, the Dhanvantree App brings essential investment tools and dedicated human support together in one convenient platform.

- Dedicated Relationship Manager Support: Get a dedicated RM after signup who understands your financial goals, assists with product selection and stays connected throughout your investment journey.

- Multiple Investment Options in One App: Explore and manage mutual funds, SIPs, fixed deposits, bonds and other financial products without switching between multiple platforms.

- Goal-Based Calculators and Portfolio Insights: Use smart financial calculators, visualise future goals and track your investments through a simplified portfolio dashboard.

- Simple Digital Onboarding and KYC: Complete your registration and KYC digitally in a few easy steps, start investing and access your portfolio anytime through the Dhanvantree App.

Other Calculators

To invest in Mutual funds you have to choose which investment option aligns with your investing strategy.

SIP Calculator

Estimate how regular monthly investments may grow over time and see the potential impact of disciplined investing.

SIP Step-Up Calculator

Discover how increasing your SIP periodically may help you build a larger corpus and achieve goals faster.

Lumpsum Calculator

Calculate the future value of a one-time investment and understand how compounding can work in your favour.

Cost of Delay SIP Calculator

See how much delaying your investment by a few months or years could cost you in the long run.

SWP Calculator

Calculate your regular monthly income from an existing investment while estimating how your remaining balance continues to grow over time.

Education Calculator

Plan for future academic milestones. Calculate the corpus required to fund your or your child’s higher education based on inflation and rising costs.

Marriage Calculator

Plan ahead for your dream wedding. Estimate the ideal investment strategy required to meet future wedding expenses without straining your finances.

How Does a Retirement Calculator Work?

A retirement calculator figures out how much your monthly lifestyle expenses will cost in the future due to inflation and estimates the total corpus required to sustain you through your life expectancy. It then factors in your existing corpus and current monthly savings to highlight any savings shortfall, telling you exactly how much extra money you need to invest via SIP or a lumpsum to cover the gap.

Unlike a simple savings calculator, it balances complex factors simultaneously: pre-retirement compound interest that grows your wealth, inflation that makes everyday expenses more expensive every year, and post-retirement returns on your remaining corpus as you draw a monthly income.

Understanding the Retirement Calculator Inputs

The retirement calculator requires a few basic inputs to map out your post-retirement financial trajectory:

Current Age: Your current age (minimum 20 years) which establishes the starting line for your investment plan.

Retirement Age: The target age when you plan to stop working (maximum 80 years), which determines your exact accumulation horizon.

Current Monthly Expenses: What you spend today to maintain your current lifestyle. The calculator uses this to estimate your future cost of living.

Expected Inflation: The annual percentage by which everyday living costs are expected to increase over time.

Current Savings Per Month: Any ongoing monthly savings you are already contributing toward retirement.

Existing Corpus: Any lump-sum money you have already accumulated or set aside for retirement before starting your new plan.

Expected Pre-Retirement Return: The annual growth rate you expect to earn on your investments during your working years (up to 30%).

Expected Post-Retirement Return: The annual growth rate you expect your corpus to continue earning after retirement as you draw down funds (up to 30%).

Life Expectancy: The estimated age until which you need your retirement corpus to comfortably last.

Example Calculation

Take the case of an individual who is currently 30 years old and plans to retire at 60. They expect to live until age 80 (a 20-year retirement period). Today, their monthly lifestyle expenses are ₹30,000. They assume a 6% inflation rate, expect a 12% pre-retirement return on investments, a 7% post-retirement return, and have an existing corpus of ₹1,00,000, while currently saving ₹5,000 per month.

From the calculator variables:

Expected Monthly Expenses at Retirement: Because of 6% inflation compounding over 30 years, the baseline lifestyle cost balloons. The monthly expense required at age 60 jumps from ₹30,000 to ₹1,72,305.

Estimated Retirement Corpus Required: To sustain a monthly payout of ₹1,72,305 for 20 years of retirement while earning 7% interest, a massive corpus of ₹3,75,41,833 is needed.

Total Savings at Retirement: Their existing ₹1,00,000 lump sum and ongoing ₹5,000/month contributions grow at 12%, yielding ₹1,91,46,039 by age 60.

Shortfall & Action Needed: This leaves a savings shortfall of ₹1,83,95,794. To bridge this remaining gap completely, the calculator reveals they need to start an additional SIP of ₹5,212 per month today, or inject an immediate lump sum of ₹6,13,923.

Benefits of Using an SIP Calculator

A Retirement calculator is not just a tool that does simple arithmetic; it is a financial roadmap with several benefits that enhance investment discipline and long-term security.

Instant and Precise Results: Provides quick estimates of your future monthly living costs and required corpus without complex manual math, conserving time and effort.

Better Investment Planning: Helps pinpoint the exact SIP or Lumpsum amount needed to securely plug your post-retirement savings shortfall.

Scenario Analysis: Enables investors to compare different scenarios by altering parameters such as retirement age, life expectancy, inflation rates, and expected returns.

Reduces Human Error: Automated accounting factors in monthly compound interest, inflation adjustments, and complex annuity drawdowns accurately without manual error.

User-Friendly and Accessible: Online retirement calculators are free, accessible anytime, and serve as an essential reality check for both young professionals and those closer to retirement.

Conclusion

A robust investment plan is necessary to achieve your long-term milestones and protect your financial independence.

A retirement calculator is a valuable tool that simplifies intricate calculations, balancing future lifestyle inflation against the potential growth of your current portfolio.

Whether you are looking to start early in your 20s to capture the magic of compounding or making mid-career corrections, a retirement calculator significantly enhances your ability to secure a dignified, self-reliant lifestyle after you stop working.

Frequently Asked Questions

A retirement shortfall is the gap between the total corpus you need to sustain your lifestyle after retirement and the estimated savings your current investments will actually generate. If the calculator shows a shortfall, you can fix it by increasing your monthly SIP, investing a one-time lump sum, extending your retirement age, or aiming for assets with a higher expected pre-retirement rate of return.

Your investment strategy changes when you stop working:

Pre-Retirement Return: The growth rate during your working years when you can generally afford to invest in wealth-building assets like equity mutual funds.

Post-Retirement Return: The growth rate during your retirement years. At this stage, most retirees shift their wealth into safer, conservative fixed-income instruments (like SWPs or debt funds) to protect capital, which typically offer a lower rate of return.

Inflation erodes the purchasing power of your money over time. A monthly lifestyle that costs ₹30,000 today will cost significantly more decades from now. By entering an inflation rate (typically between 5% and 7%), the calculator ensures that your target corpus is large enough to buy the exact same standard of living in the future that you enjoy today.

Yes. You can alter the Retirement Age field to a younger age (e.g., 45 or 50). The calculator will automatically shrink your wealth accumulation timeline and increase your life expectancy period, showing you exactly how much more you need to save per month to achieve financial independence early.