ITR Filing AY 2026-27: Deadlines, Section 87A Rebate, and Every Rule You Need to Know

Introduction

Missing your ITR filing deadline by even a day can cost you the right to carry forward losses. Earn ₹1 more than a key threshold, and a ₹60,000 tax rebate disappears entirely. Income Tax Return filing isn’t just paperwork, it’s a system of thresholds, defaults, and deadlines that quietly work for you or against you, depending on whether you understand them.

This article covers everything you need for Assessment Year 2026-27 (Financial Year 2025-26) exact deadlines by taxpayer category, how the Section 87A rebate can bring your tax bill to zero, the New Tax Regime default rules, common filing mistakes, and a pre-filing checklist you can run through before you submit.

What Is the ITR Filing Last Date for AY 2026-27?

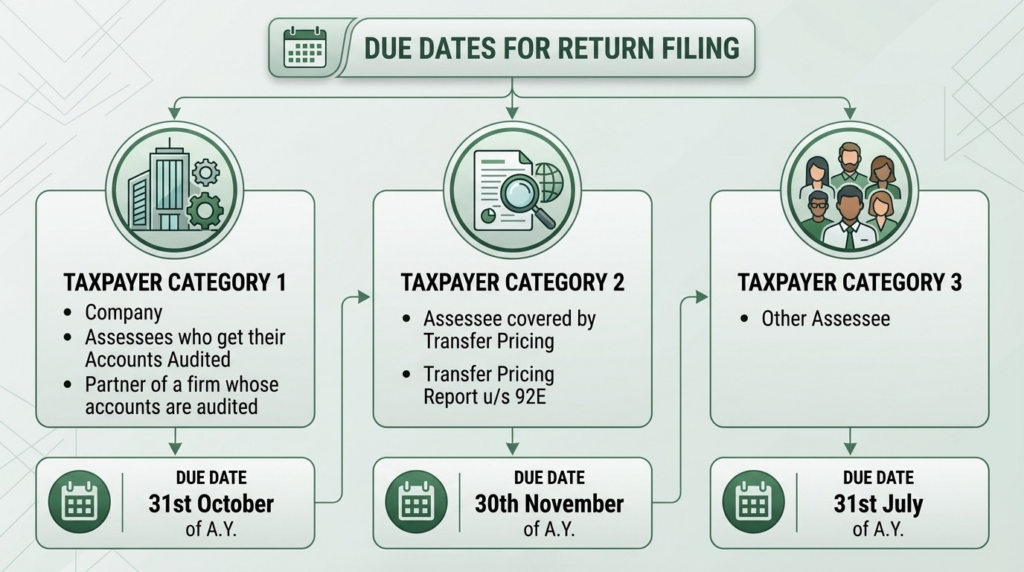

For most individual taxpayers, the ITR filing last date is 31 July 2026. Businesses and professionals not requiring an audit get until 31 August 2026, audit cases have until 31 October 2026, and belated returns can be filed up to 31 December 2026 though with real trade-offs, explained below.

ITR Filing Due Dates for AY 2026-27 (Full Table)

Your deadline depends on your taxpayer category and the ITR form you file, not a single universal date.

For the first time, non-audit business and professional taxpayers filing ITR-3 or ITR-4 get a full extra month beyond the salaried deadline, a meaningful change if that’s your category.

The Real Cost of Filing a Belated Return

Filing late isn’t just about a penalty fee. It comes with two consequences that are easy to overlook:

- You lose the right to carry forward capital or business losses to future assessment years.

- You’re automatically locked into the New Tax Regime with no option to switch to the Old Regime, even if it would have reduced your tax bill.

If either of those applies to you, treat July or August not December as your real deadline.

A Quiet Legal Shift Behind This Year's Filing

This filing season sits at a transition point. The new Income Tax Act, 2025 came into force on 1 April 2026 but since AY 2026-27 covers income earned before that date (FY 2025-26), your return this year is still governed entirely by the older Income Tax Act, 1961. Nothing about how you calculate or file has changed yet. That shift only applies from Tax Year 2026-27 onward, with returns due in 2027.

New Tax Regime vs Old Tax Regime: Understanding the Default

Here’s something many taxpayers still get wrong: if you file without actively choosing otherwise, you’re taxed under the New Tax Regime by default. HRA, Section 80C, Section 80D none of the traditional deductions apply unless you actively opt out.

- If you’re salaried with no business income: you can switch between the Old and New Regime every single year, directly within your ITR, as long as you file by the due date.

- If you have business or professional income: that flexibility disappears. To use the Old Regime, you must file Form 10-IEA on the e-filing portal before your due date. And once you switch back to the New Regime, you can only do it once in your lifetime.

Section 87A Rebate Explained: How to Pay Zero Income Tax on Your ITR Filing

Before the numbers, one distinction matters: a deduction reduces your taxable income before tax is calculated. A rebate wipes out the tax you’ve already calculated. Section 87A is a rebate and used correctly, it can bring your final tax liability to zero.

Section 87A Rebate Limits for FY 2025-26 (AY 2026-27)

Financial circumstances and goals can evolve. Periodic reviews help investors assess whether their mutual fund holdings continue to align with their objectives and requirements.

Tax Regime | Income Limit | Maximum Rebate |

|---|---|---|

Old Regime | ₹5,00,000 | ₹12,500 |

New Regime | ₹12,00,000 | ₹60,000 |

Why Salaried Employees Can Earn Up to ₹12.75 Lakh Tax-Free

The New Regime’s Standard Deduction of ₹75,000 stacks directly with the Section 87A rebate. Run the math, and a salaried employee earning up to ₹12,75,000 gross can end up paying zero income tax: the ₹75,000 deduction brings net taxable income down to exactly ₹12,00,000, and the ₹60,000 rebate erases the tax on that amount entirely.

The ₹1 Cliff and How Marginal Relief Protects You

Think of the tax rebate as a steep cliff rather than a gentle slope. If you earn exactly ₹12,00,000, you get a full ₹60,000 tax rebate (meaning you pay zero tax). But if you earn just ₹1 more (₹12,00,001), that entire ₹60,000 discount vanishes instantly, not just the tax on that extra ₹1.

Without a safety net, this rule would actually punish you for making more money, leaving you with less take-home pay than someone who earns less than you.

To fix this unfair jump, the government uses a rule called Marginal Relief. It acts as a shield, making sure that your extra tax is never higher than the extra income that pushed you over the ₹12 lakh limit.

Who Cannot Claim the Section 87A Rebate

The Section 87A rebate is available only to resident individuals. It cannot be claimed by non-residents, companies, partnership firms, or Hindu Undivided Families (HUFs).

The rebate also does not apply to certain types of income that are taxed at special rates. For example:

- Short-Term Capital Gains (STCG) under Section 111A, which are taxed at 20%.

- Long-Term Capital Gains (LTCG) on listed equities are tax-free up to ₹1.25 lakh per financial year under Section 112A. Any profit above this limit is taxed at a flat rate of 12.5%.

This means that even if your total income is within the rebate limit, you may still have to pay tax on these types of capital gains.

What's New in the ITR Forms for AY 2026-27

A few form-level changes are worth confirming before you start filing, since using the wrong form can get your return flagged as defective:

- ITR-1 now covers up to two house properties, not just one a genuine simplification for salaried filers with a second home. A third property still requires ITR-2.

- Company directors must file ITR-2 or ITR-3, ITR-1 isn’t an option for them.

- Agricultural income over ₹5,000 also pushes you out of ITR-1.

- Schedule AL (Assets & Liabilities) disclosure is now only mandatory above ₹1 crore total income, a relief for taxpayers who previously had to itemize assets at a lower threshold.

- ITR-2 now includes a separate field for reporting buyback-related capital losses, helping taxpayers disclose these transactions correctly under the revised tax rules.

Common ITR Filing Mistakes to Avoid

1. Missing Income the Tax Department Already Knows About

Savings account interest, fixed deposit interest, dividends, rental income, and capital gains are the most frequently overlooked income sources and they are not actually hidden. The Income Tax Department tracks all of this through your Annual Information Statement (AIS) and Form 26AS. Miss even a small interest payout, and an automated mismatch notice under Section 143(1) is often just a matter of time.

2. Trusting Pre-Filled Data Without Checking It

The e-filing portal now pre-fills more of your return than ever, pulling data from the AIS, stock depositories, and banking institutions. While convenient, this system is not infallible. Duplicate entries or incorrect transaction classifications can happen. Always cross-check pre-filled values against your personal bank statements, capital gains reports, and tax credit certificates before clicking submit.

3. Waiting Too Long When Form 16 Is Delayed

Don’t let a slow employer turn into a rushed, last-minute filing. If your Form 16 is delayed:

- Download your AIS and Form 26AS from the e-filing portal to verify your recorded Tax Deducted at Source (TDS).

- Reconcile your monthly payslips against actual bank credits to accurately reconstruct your gross salary.

- Gather your investment and deduction proofs early, especially if you are planning to opt out of the default regime.

- If numbers still do not match, use the portal’s feedback system to dispute incorrect AIS entries before submitting.

4. Failing to Disclose All Active Bank Accounts

Many taxpayers mistakenly believe they only need to report the primary bank account where they receive their salary or business income. By law, you must disclose every single active bank account held in India in your name at any time during the financial year (excluding truly dormant accounts that have been inactive for over two years). Crucially, ensure that at least one primary account is pre-validated on the portal, or your tax refund cannot be electronically credited.

5. Blindly Copying "Book Profits" for Business Returns (ITR-3 & ITR-4)

If you have business or professional income, a frequent mistake is assuming that your standard accounting profits match your taxable profits. For tax purposes, you must reconcile your books with the Income Computation and Disclosure Standards (ICDS). Differences in how ICDS mandates inventory valuation, revenue recognition, or depreciation mean that your business ledger profits must almost always be adjusted before they are entered into your ITR.

6. Choosing the Wrong Tax Form

Using the wrong ITR form can cause your return to be flagged as defective under Section 139(9). For instance, while ITR-1 is the default for salaried individuals, you are legally barred from using it if you own more than two house properties, have agricultural income exceeding ₹5,000, hold unlisted equity shares, or serve as a director in a company. Take a moment to verify your specific income streams against the criteria for ITR-1, ITR-2, or ITR-3 before initiating the form utility.

ITR Pre-Filing Checklist

Run through this before you hit submit:

- Compared Old vs. New Regime outcomes using current Standard Deduction figures (₹75,000 vs ₹50,000)

- Filed Form 10-IEA before the due date, if opting for the Old Regime with business/professional income

- Confirmed you’re using the correct ITR form for your income sources

- Cross-checked pre-filled data against your own AIS, Form 26AS, and personal records

- Separated special-rate capital gains (Sections 111A, 112A) to confirm the 87A rebate is calculated correctly

- Filing before your July/August deadline, if carrying forward losses matters to you

- Pre-validated your refund bank account on the e-filing portal

Why Filing Your ITR On Time Pays Off (Even If You Earn Below the Tax Slab)

If your income is below the tax slab, you might think you don’t need to file an Income Tax Return (ITR). However, filing a “Nil ITR” (a return showing zero tax owed) on time acts as a powerful financial tool.

Here is how a clean, timely filing history helps you in the long run:

1. Your Losses Become an Asset, Not a Dead End

If you lose money in business or the stock market, those losses don’t have to vanish into thin air. If you file your ITR on time, the government allows you to carry forward these losses for future years. This means when you make a profit next year, you can subtract this year’s losses from it, drastically lowering your future tax bill. If you file late, you lose this privilege entirely.

2. Loans Move Much Faster

When you apply for a home, auto, or business loan, banks look at your financial discipline. Lenders typically expect to see 2 to 3 years of consistent, clean ITR history to verify your income stability. If you haven’t been filing because you were under the tax slab, the bank has no official paperwork to trust, which can delay or completely stall your loan approval.

3. It's Your Only Route to Get a Refund

Sometimes, a client or an employer might deduct Tax Deducted at Source (TDS) from your payouts, or you might have overpaid advance tax. If your total income for the year ends up being under the tax slab, that deducted money actually belongs to you. However, the government won’t just send it back automatically; the only way to get your refund is by filing an ITR.

4. Visa Officers Pay Attention

When you apply for a visa to travel or study abroad, embassies want proof that you have deep roots and financial stability in India. A steady, consecutive history of filing your ITR even if it shows a low income is read by visa officers as official evidence that you are a law-abiding, financially trackable citizen.

5. It Builds Your Business Credibility

A consistent filing history serves as an informal certificate of credibility in the professional world. If you ever want to apply for government tenders, enter corporate partnerships, or sign commercial property leases, a clean track record of timely ITR filings proves that your background is stable and transparent.

Conclusion

Income Tax Return filing is more than an annual compliance requirement; it is an important part of maintaining a healthy financial record. Understanding the applicable deadlines, choosing the appropriate tax regime, verifying information before filing, and staying updated with changes in tax regulations can help taxpayers avoid unnecessary complications and complete the filing process with greater confidence.

Dhanvantri Capital Services Pvt. Ltd. is an AMFI-registered Mutual Fund Distributor (ARN-194216) believes that improving financial awareness is an essential step toward better financial decision-making. Through educational articles, investor awareness initiatives, and simplified explanations of important financial and regulatory developments, we aim to make complex financial topics easier to understand for investors.

Whether you’re filing your first Income Tax Return or reviewing the latest changes for AY 2026–27, staying informed and referring to reliable sources can make the process smoother and more efficient. As tax laws and regulations continue to evolve, readers are encouraged to verify the latest information on the official Income Tax e-Filing portal and consult a qualified Chartered Accountant or tax professional whenever required.

Disclaimer: Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. This article is intended solely for educational and informational purposes and should not be construed as investment advice, financial advice, legal advice, or a recommendation to invest in any product or strategy.

Table of Contents

Frequently Asked Questions

31 July 2026 for salaried individuals and pensioners; 31 August 2026 for freelancers and professionals without audit requirements; 31 October 2026 for audit cases.

Yes, as a belated return, up to 31 December 2026 — but you’ll lose the ability to carry forward certain losses and won’t be able to switch to the Old Regime if you have business or professional income.

₹60,000 under the New Regime for taxable income up to ₹12,00,000, and ₹12,500 under the Old Regime for taxable income up to ₹5,00,000.

If you have business or professional income and want the Old Regime, yes it must be filed before your due date each year you want to opt out of the New Regime default.

No. It doesn’t apply to income taxed at special rates, including Short-Term Capital Gains under Section 111A or Long-Term Capital Gains under Section 112A.

Leave a Reply